FHLB for Insurers: A Source of Liquidity During Market Dislocations

June 13, 2023

By John Rup, Vice President, and Matthew Reilly, Managing Director, Institutional Solutions

As funding costs rise, credit markets are stressed and investors are distressed, insurers accustomed to a period of low rates may be left wondering what to do next. In response, Conning would suggest insurers consider options to strengthen their balance sheets; one may be a membership with a Federal Home Loan Bank (FHLB).

FHLB membership could be a valuable benefit for insurers as its borrowing programs may help enhance profitability, balance sheet strength and financial stability. FHLB membership is growing among larger insurers and Conning believes it merits further consideration from mid-size companies as well.

Founded in 1932 in response to the Great Depression to support homeownership and distressed lenders, the FHLB system has become increasingly popular as a financing option among insurers. Insurance companies can use the FHLB system and its competitive borrowing rates for emergency short-term liquidity backstops, funding for working capital or strategic investments (including mergers and acquisitions), aid in asset liability management, or potentially generating additional net investment income through spread-investing programs.

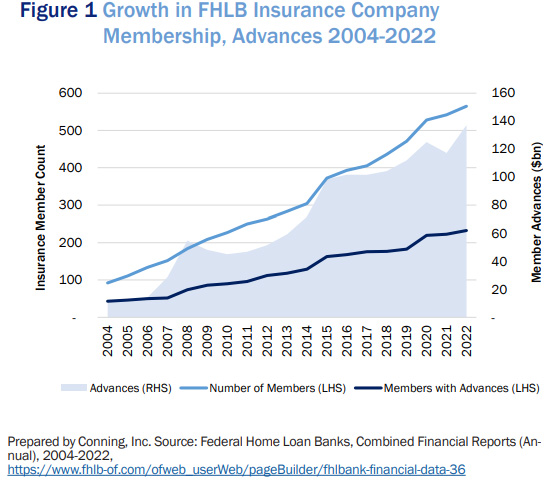

A growing number of insurance companies are looking to take advantage of FHLB programs, as witnessed by the continuing increase in its membership rate and borrowing activities (see Figure 1). At year-end 2022, 565 insurance companies were FHLB members, up from 405 at year-end 2017. During that same period, the total principal of outstanding advances to insurers rose to $137 billion from $104 billion, a 6% annual growth rate.1

Click below to continue reading Conning’s Viewpoint, “FHLB for Insurers: A Source of Liquidity During Market Dislocations."

Footnotes

1 FHLBank Combined Annual Report, 2022 Year-End; https://www.fhlb-of.com/ofweb_userWeb/resources/2022Q4CFR.pdf

Disclosure

©2023 Conning, Inc. This document and the software described within are copyrighted with all rights reserved. No part of this document may be distributed, reproduced, transcribed, transmitted, stored in an electronic retrieval system, or translated into any language in any form by any means without the prior written permission of Conning. Conning does not make any warranties, express or implied, in this document. In no event shall Conning be liable for damages of any kind arising out of the use of this document or the information contained within it. This document is not intended to be complete, and we do not guarantee its accuracy. Any opinion expressed in this document is subject to change at any time without notice. Conning, Inc., Goodwin Capital Advisers, Inc., Conning Investment Products, Inc., a FINRA-registered broker-dealer, Conning Asset Management Limited, Conning Asia Pacific Limited, Octagon Credit Investors, LLC, Global Evolution Holding ApS and its group of companies (“Global Evolution”), and Pearlmark Real Estate, L.L.C. are all direct or indirect subsidiaries of Conning Holdings Limited (collectively, “Conning”) which is one of the family of companies owned by Cathay Financial Holding Co., Ltd., a Taiwan-based company. Conning has investment centers in Asia, Europe and North America. C: 16956529